In this week’s blog, we’ll cover provisional income and gain a better understanding of what effect this will have on the taxation of your Social Security.

Up until 1984, Social Security benefits were explicitly excluded from federal income taxation. However, in 1983 legislation was passed to implement a taxation on up to 50% of your Social Security benefit based on your “provisional income.” Depending on your filing status, married or single, there were income thresholds put in place to dictate who would be subject to their benefit being taxed.

Legislation enacted in 1993 extended taxation of benefits. The legislation increased the limitation on the amount of benefits subject to taxation from 50% to 85% for single and married taxpayers that were subject to a higher income threshold.

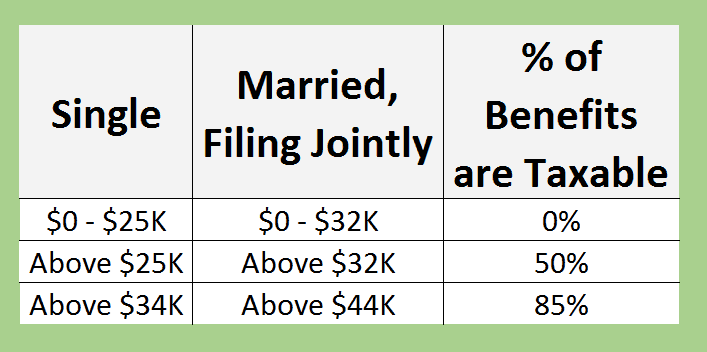

Below is a chart that illustrates the income thresholds that were passed into law:

As we stated earlier, these thresholds are subject to your “provisional income”. So, what is provisional income? Your provisional income is made up of your adjusted gross income, plus any non-taxable interest (such as municipal bond income), and finally half of your Social Security benefit. Add all of these up, and this is your provisional income. Once you have calculated your income, you can now figure out where you land on the chart above which will let you know how much of your benefit is going to be taxed.

Having an understanding of Social Security and the taxation of it can help you better plan for retirement. Now that you know how much and when Social Security is going to be taxed, you can better plan on when to file for Social Security.

For example, if you’re an individual who is planning on working past full retirement age (FRA), it may make sense to delay your benefit until after you separate from your employer. We would assume at that point your provisional would be lower, which means less of your Social Security is taxed. In addition, as covered in our previous blog, you also know that for every year you delay taking your benefit past FRA, you will receive a permanent 8% increase in your benefit. In this example, by delaying Social Security you would avoid the bulk of your benefit being taxed as you haven’t yet filed, and additionally you also increased your benefit for the remainder of your life.

Over the past few weeks, we’ve covered the ins and outs of Social Security which has highlighted just how much there is to consider and plan for in regard these benefits. With that being said, it’s always important to consult with a professional to better understand what’s going to be the best strategy based on your unique situation, as everyone’s scenario is going to be different.

Ben Webster, CFP® and Derek Prusa, CFA, CFP®

Co-Founders and Owners of Aspire Wealth

How Working Affects Social Security Benefits